Having said that, there are two reasons for believing that valuations may be drifting higher with time, which would require long-term forecasters to make some adjustments to their models. First, there is no doubt that the cost of buying and holding equities has fallen dramatically over time. For example, I remember buying the closed-end , NYSE-traded The Mexico Fund in the mid-1990s. Trading commissions were in the order of ten times the $5/trade many brokers charge today, the fund manager charged a management fee well above 2% for what was essentially an index fund. To top it off, the fund traded at very large discounts to Net Asset Value, sometimes as great as 30%. Compare that to the emerging market country funds now trading in ETF form with annual fees of as low as 14 basis points (0.14%), and it is clear that investing in emerging market equities, as in other asset classes, has never been cheaper than today. It would make sense that valuations would at least partially reflect the lower transaction costs.

Another often-cited, though less plausible, explanation for higher valuations is that risk has been permanently reduced by lower economic volatility. This theory was advanced as a possibility already in the late 1950s by no less than the legendary investor and teacher Ben Graham, who was searching for a reason to explain why U.S. stocks had appreciated so much during the post-war period. If one believes Ben Bernanke’s theory that improvements in the science of monetary economics has resulted in a “great moderation,” or smoothing of economic cycles, than this could point to higher-for-ever valuations. Of course, one would have to explain the Great Financial Crisis of 2008-2009 as a “Five Sigma” event not likely to happen for another thousand years. This is the view that has been publicly expressed rather unconvincingly, in my view, by Bernanke and Janet Yellen, and which justifies the extremely low volatility and high valuations of the current investment environment.

What does history tell us about current valuations? The work of GMO, Research Affiliates, and Haussman all agree that most assets priced at levels that point to very low expected returns for most asset classes.

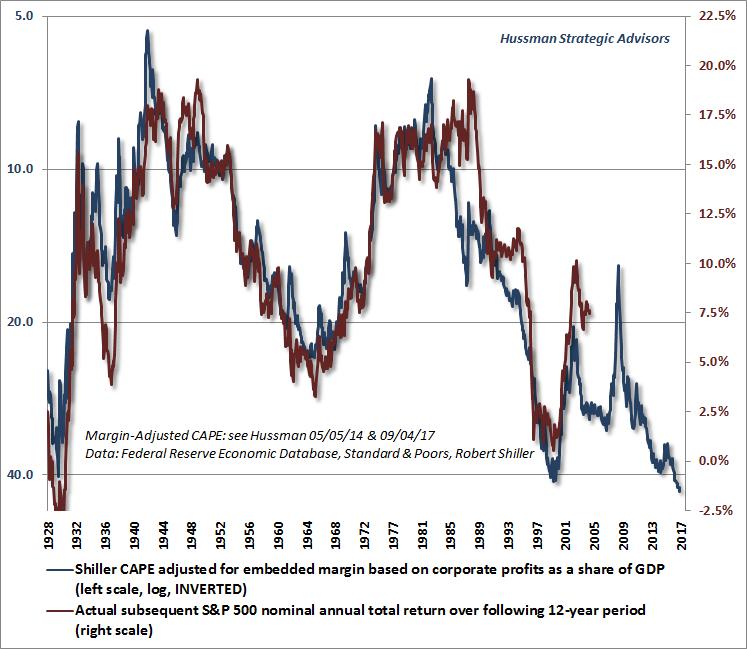

First, let’s look at the work of John Hussman (Hussman Funds), which back-tests historical data to forecast future returns. Hussman’s model predicts negative 2% nominal (including inflation) returns for the next 12 years.

{kind=link}

Second, let’s look at GMO, which has made these forecasts for decade with a high degree of predictive success. The table below shows GMO 7-year forecast for real (inflation-adjusted) returns. GMO sees negative returns for stocks, partuclarly U.S. large cap stocks with negative 4.6% annual real returns (in line with Hussman’s number). Emerging markets stocks are the exception, priced to give a 2.2% real annual return. Jeremy Grantham, GMO Chief Strategist, recently advised his clients to load-up as much as they can on emerging market equities.

Third, we look at Research Affiliates, with the results of their latest exercise below. RA forecasts real returns and volatility for the next ten years. RA’s model points to generally higher returns for all asset classes compared to GMO’s, but still U.S. equities are expected to provide near zero return for the period. International returns (EAFE, Europe, Asia, ar-East) are slated at slightly above 4%, and emerging markets are expected to provide real returns of 6% per year.

These three approaches point to relatively high expected returns for emerging markets. These can be explained by three factors: 1.relative under-performance over the past five years; 2.Valuations in line with history, and quite low relative to U.S. equities; 3. the earnings cycle; and 4. the currency cycle.

- Relative Underperformance (S&P 500 vs. MSCI Emerging Markets Index)

- Valuations (Cyclically Adjusted PE ratio), S&P500 vs. EM

3.Earnings are on the rebound in EM.

4.Competitive Currencies

Fed Watch:

- Will wealth inequality end the bull market (Tony Isola)

- The rate of return on everything (NBER)

- Globalrisk-free rate hits 88-year low (Bank of England)

India Watch:

- India’s bond rout (Bloomberg)

- India wearily eyes tech (MIT Tech Review)

China Watch:

- US politics gets in the way of Ant Financial’s US plans (SCMP)

- Making China Great Again (The New Yorker)

China Technology Watch:

- Chinese tech workers are flocking home (Bloomberg)

- How China went from made in to created in (SCMP)

- China’s hypersonic weapons (Geopolitical Futures)

- Baidu’s open-source software for self-driving cars (Tech Review)

EM Investor Watch:

- Pakistan ditches the dollar for China trade (CNBC)

- The end of the Asian miracle (Project Syndicate)

- A few thoughts on EM investing (Fortune financial)

Technology Watch:

- Apple’s share of smartphone profits is falling (SCMP)

- Fanuc’s robots are changing the world (Bloomberg)

- Battery costs coming down (Bloomberg)

Investor Watch:

- Shiller on narrative (Chicago Booth)

- The coming melt-up in stocks (GMO)

“The central truth of the investment business is that investment behavior is driven by career risk. In the professional investment business we are all agents, managing other peoples’ money. The prime directive, as Keynes knew so well, is first and last to keep your job. To do this, he explained that you must never, ever be wrong on your own. To prevent this calamity, professional investors pay ruthless attention to what other investors in general are doing. The great majority ‘go with the flow,’ either completely or partially. This creates herding, or momentum, which drives prices far above or far below fair price. There are many other inefficiencies in market pricing, but this is by far the largest. It explains the discrepancy between a remarkably volatile stock market and a remarkably stable GDP growth, together with an equally stable growth in ‘fair value’ for the stock market.” ~ Jeremy Grantham